3-D Secure (short for Three Domain Secure), is an extra level of security to ensure that every transaction done with your card is authorized by you. This is put in place to reduce fraudulent activities for Card Not Present (CNP) transactions.

What are CNP transactions?

Card Not Present transactions are card payments made where the cardholder does not, or cannot physically present the card at the point of payment. These type of transactions are commonly made over the Internet.

It is easy to get your debit card lost, or the information on it compromised. Likewise, if your computer or mobile phone is lost or stolen and if any of these devices hold your card information you can be exposed. This is where 3-D Secure comes in, it is an added layer of security can prevent the fraudulent use of your card. To authorise a transaction via 3-D Secure, you will be required to provide personal information that only you (the card owner) should know. This means that you are the only person able to authorise transactions with your card, except this personal information is somehow compromised.

There are three parties involved in the 3-D Secure process:

- The Payment Gateway – Paystack.

- The Card Network – Visa, MasterCard or Verve.

- The Issuing bank – The customer's bank that issued the card

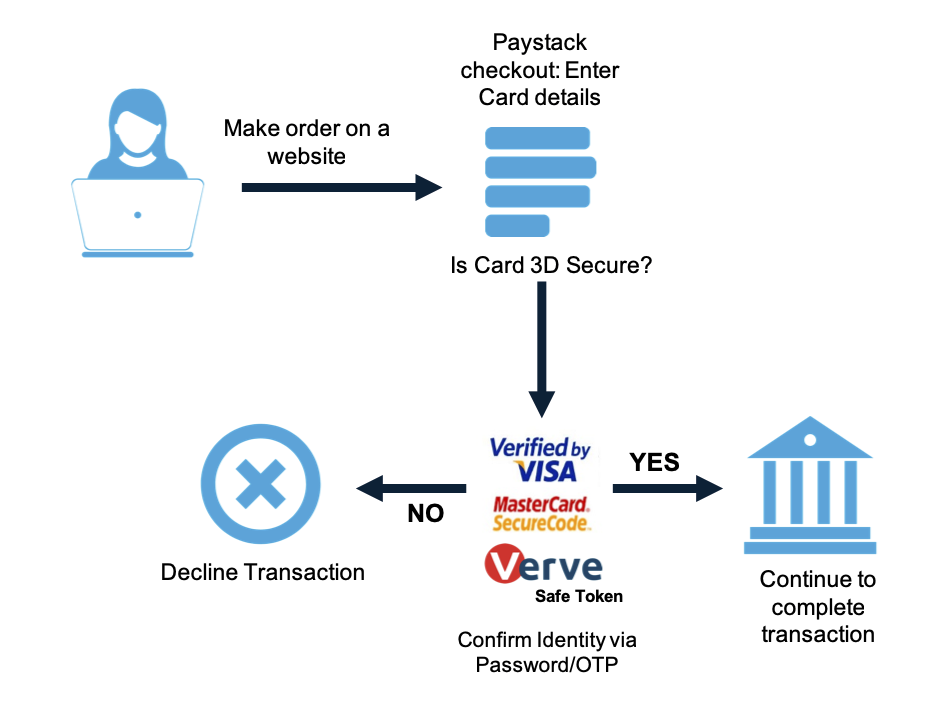

Here is a graphic to explain the payment process with 3-D Secure:

3-D Secure is also important to the business owner

The presence of 3-D Secure on Paystack transactions means that the business owner has reduced liability. This is because verified transactions have better protection against chargebacks. It increases the likelihood that this transaction was authorised by the owner of the card and even if it was not, your business may not bear the loss after you have provided value.

Are there limitations to 3-D Secure?

3-D Secure is a proven technology to combat fraud. But, this does not mean that business owner cannot get away with fraud themselves. For example, 3-D Secure cannot control whether a business owner offers adequate value to the customer for a payment they've made. If as a customer, you did receive what you paid for, or you are very dissatisfied with what you got, you can file a chargeback at your bank.

Will this increase the number of failed transactions?

Not necessarily. The aim of 3-D Secure is to add an extra layer of security, for the cardholder, not to affect success rates. However, if the card is not activated for 3-D Secure, or there is a mistake in the authentication process, the transaction will fail.

What if I don't want 3-D Secure, can I turn 3-D Secure off?

3-D Secure authentication for online transactions is a compliance requirement for our transactions so it can't be turned off.

How do I activate my account for 3-D Secure?

Card issuers (e.g. your bank), largely have upgraded their systems to enroll their customers to 3-D Secure. Also, most cards are automatically signed up for 3-D Secure. If your MasterCard or Visa is not 3-D Secure enabled, please contact your bank. They can activate your card, and you will get a PIN that will enable you to perform transactions anywhere.

Comments

0 comments

Article is closed for comments.