You can respond to chargebacks from your Paystack Dashboard on the Disputes page of the Dashboard. This provides an interface where you can properly track and manage your chargeback claims.

You can respond to a chargeback either by accepting, or declining the claim. Here are what it means to do either:

Accepting a chargeback: This means you successfully received the customer’s payment but did not provide the service or product the customer paid for. This could be for several different reasons due to technical issues or human error. When you accept a chargeback, you allow for the funds to be deducted from your payouts and reversed to the customer’s bank account.

Paystack doesn't charge you a penalty when you accept a chargeback, however, the full transaction amount is reversed to the customer's bank account once the chargeback is accepted.

Declining a chargeback: This means you successfully received the customer’s payment and have provided a service or delivered the product to the customer. To justify this, you will need to upload a form of evidence to support your claim, such as a receipt or invoice, anything that proves value was provided. If the evidence is not sufficient, we will automatically accept the chargeback.

Find below an illustration of how to respond to chargebacks:

What kind of evidence should I provide to decline a Chargeback?

This varies depending on the type of business you're into, as different businesses give value in various ways. However, whatever document you upload as evidence should have the following:

- The name of the customer who initiated the transaction as stated in their identification document

- The disputed transaction amount

- The first six and last four digits of the card used to make the payment (for card transactions)

- The date the disputed sum was successfully paid and received by you

- A brief description of the goods or service delivered to the customer

The quality of your receipt is highly dependent on the KYC (Know Your Customer) requirements you've set for your business. With a strong KYC system in place, you'll be able to identify who you're transacting with and provide accurate information about them if the need arises. Click here to learn more about KYC.

Here are some decline evidences that can serve as a guide:

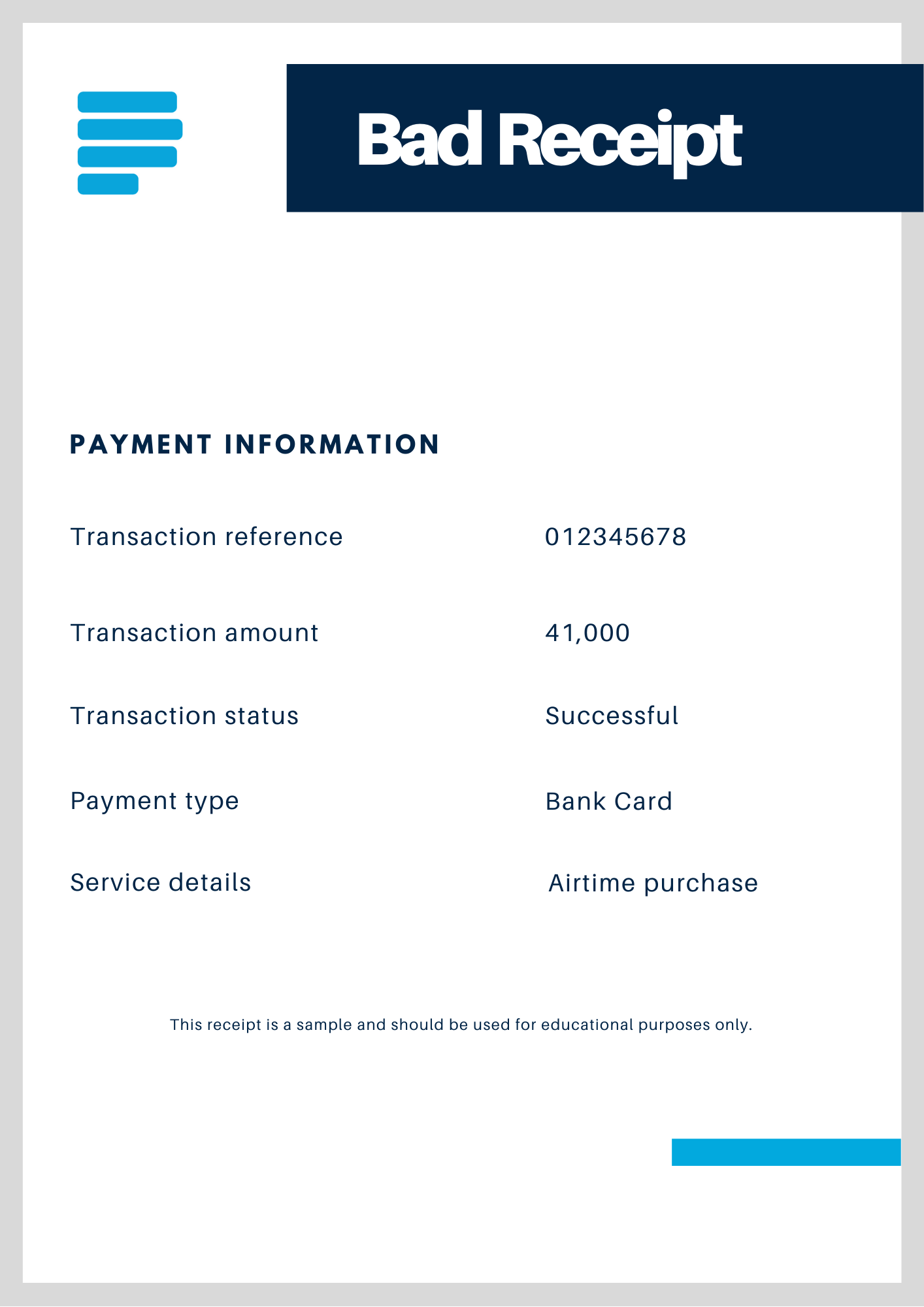

This is an example of a bad receipt because it contains no information that can identify the customer

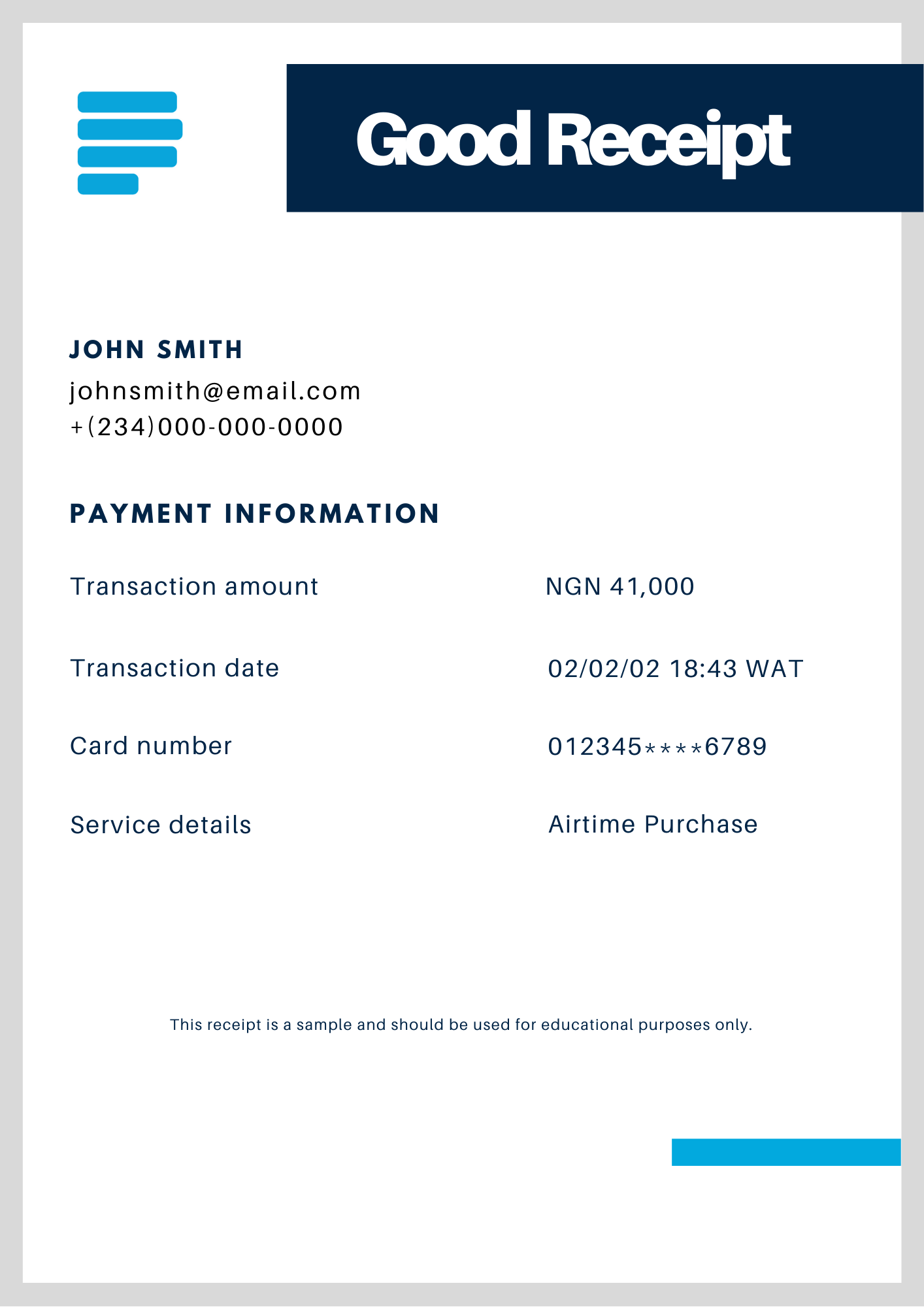

This is an example of a good receipt because it contains the customer name, email and phone number

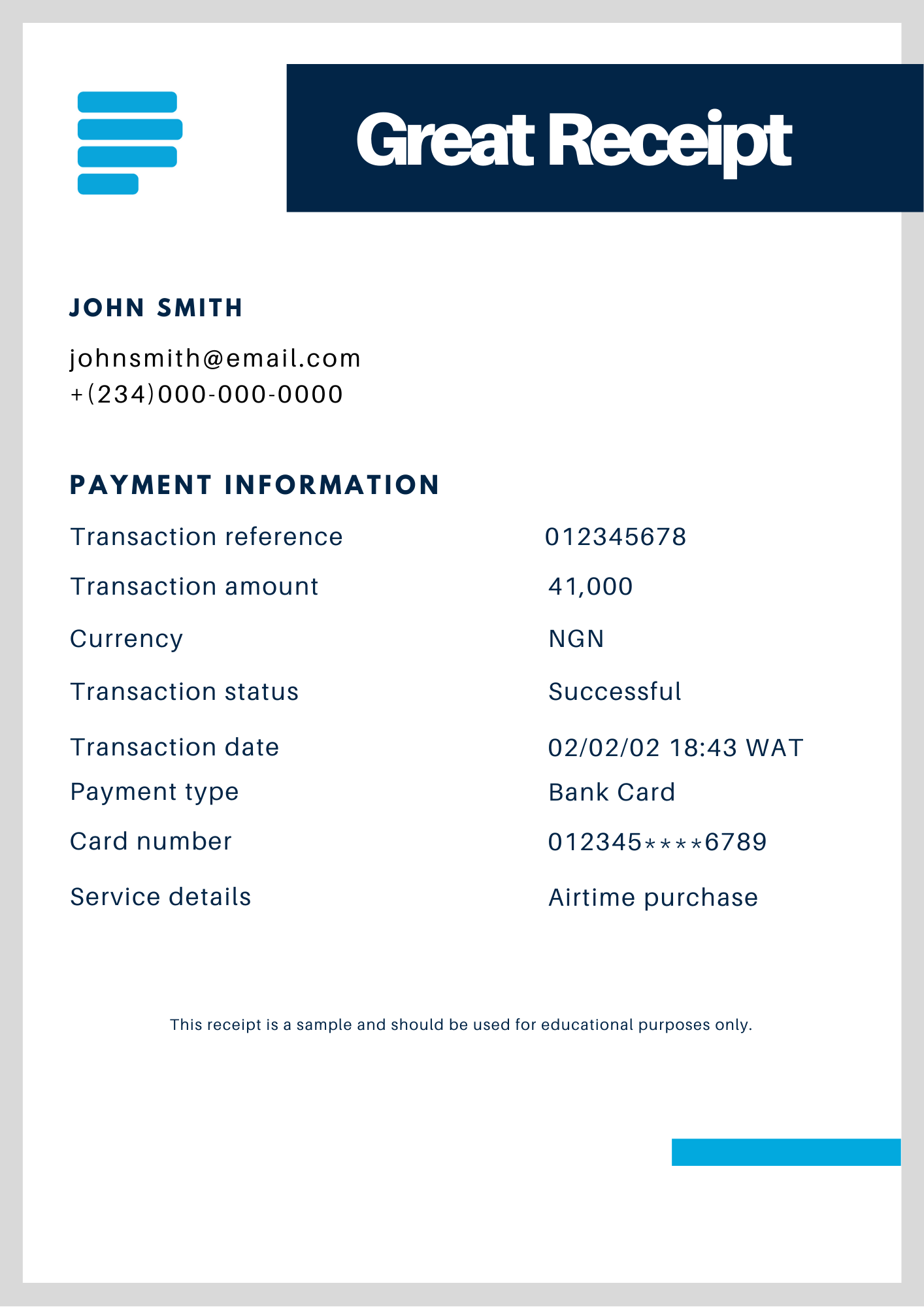

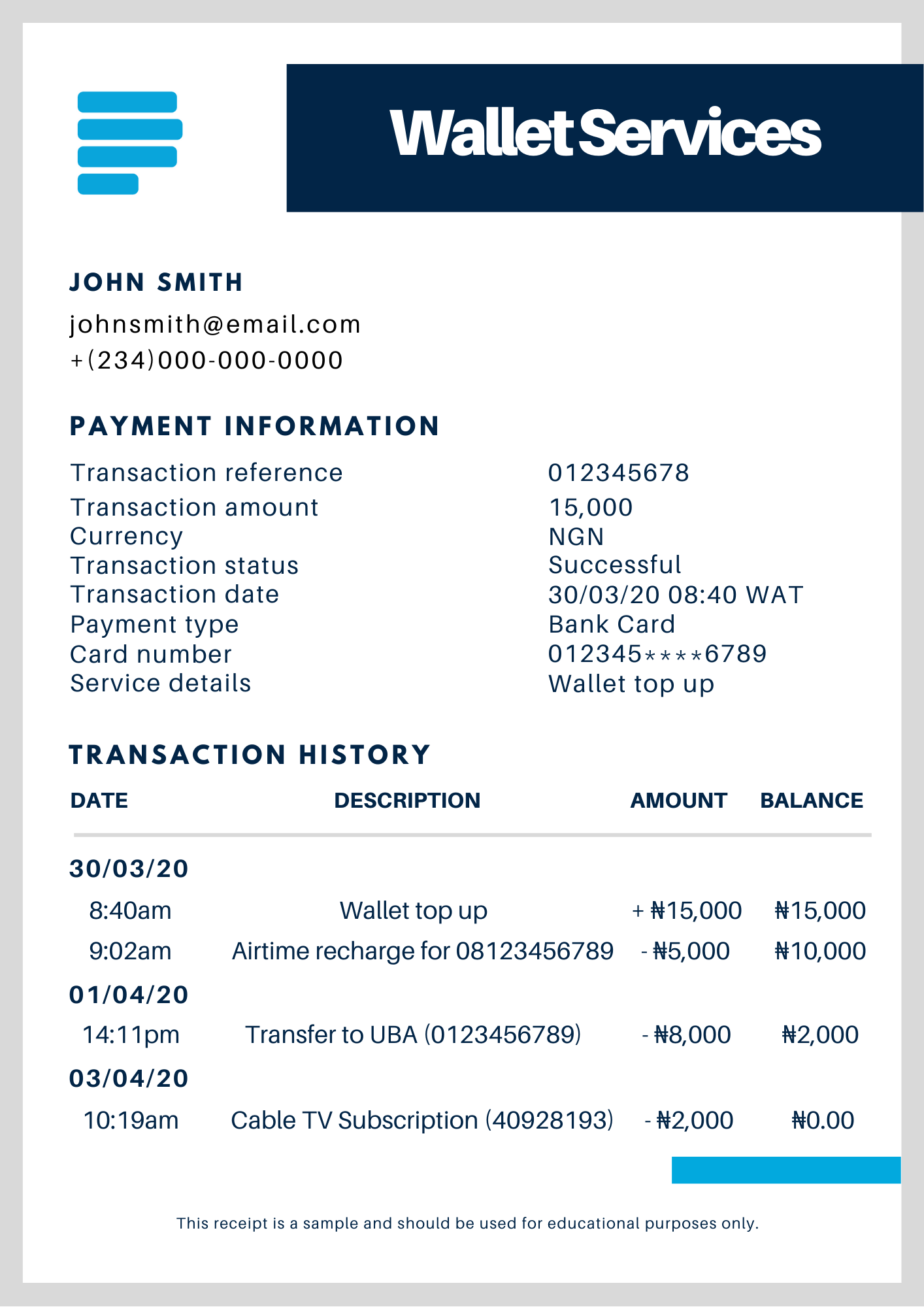

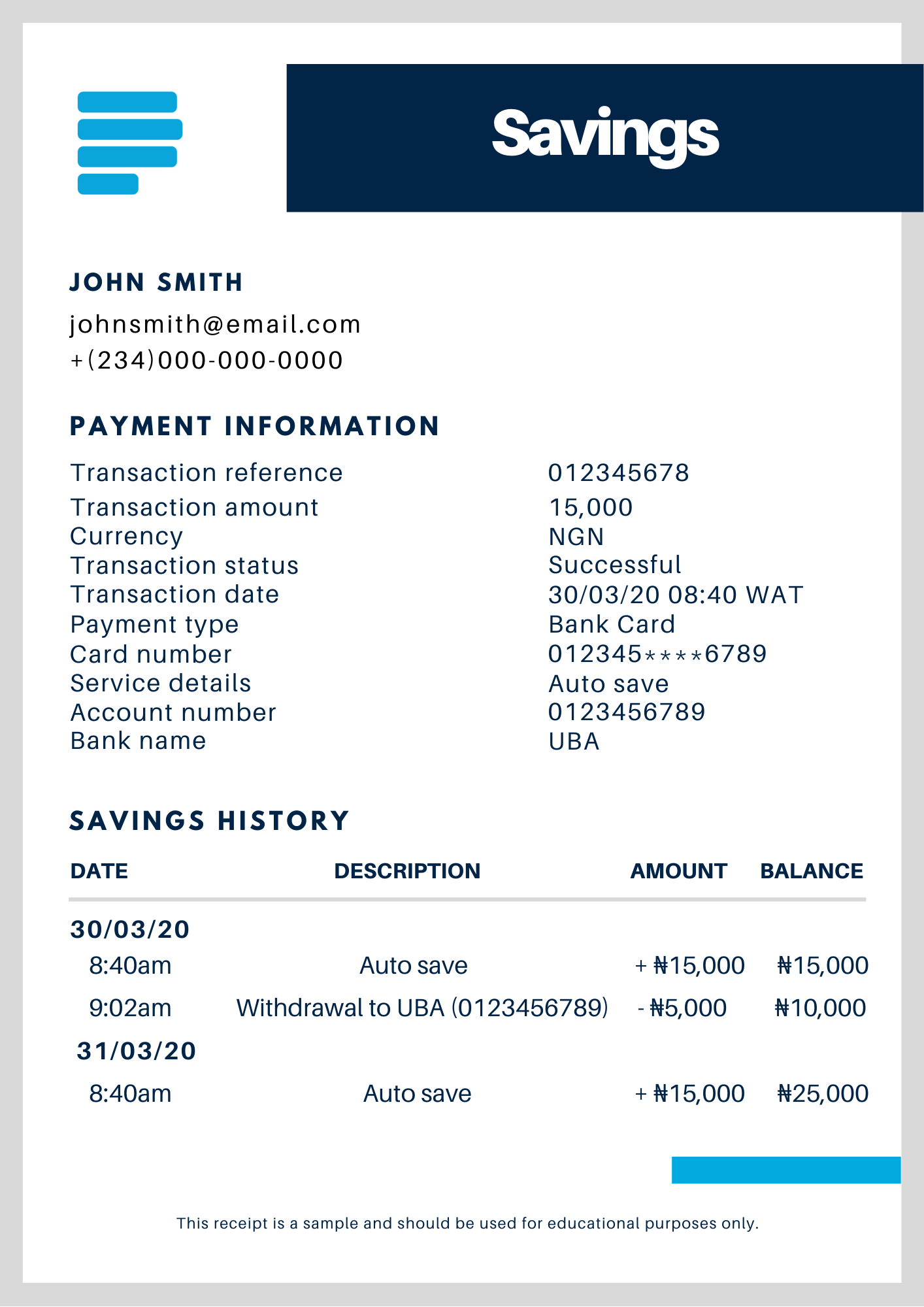

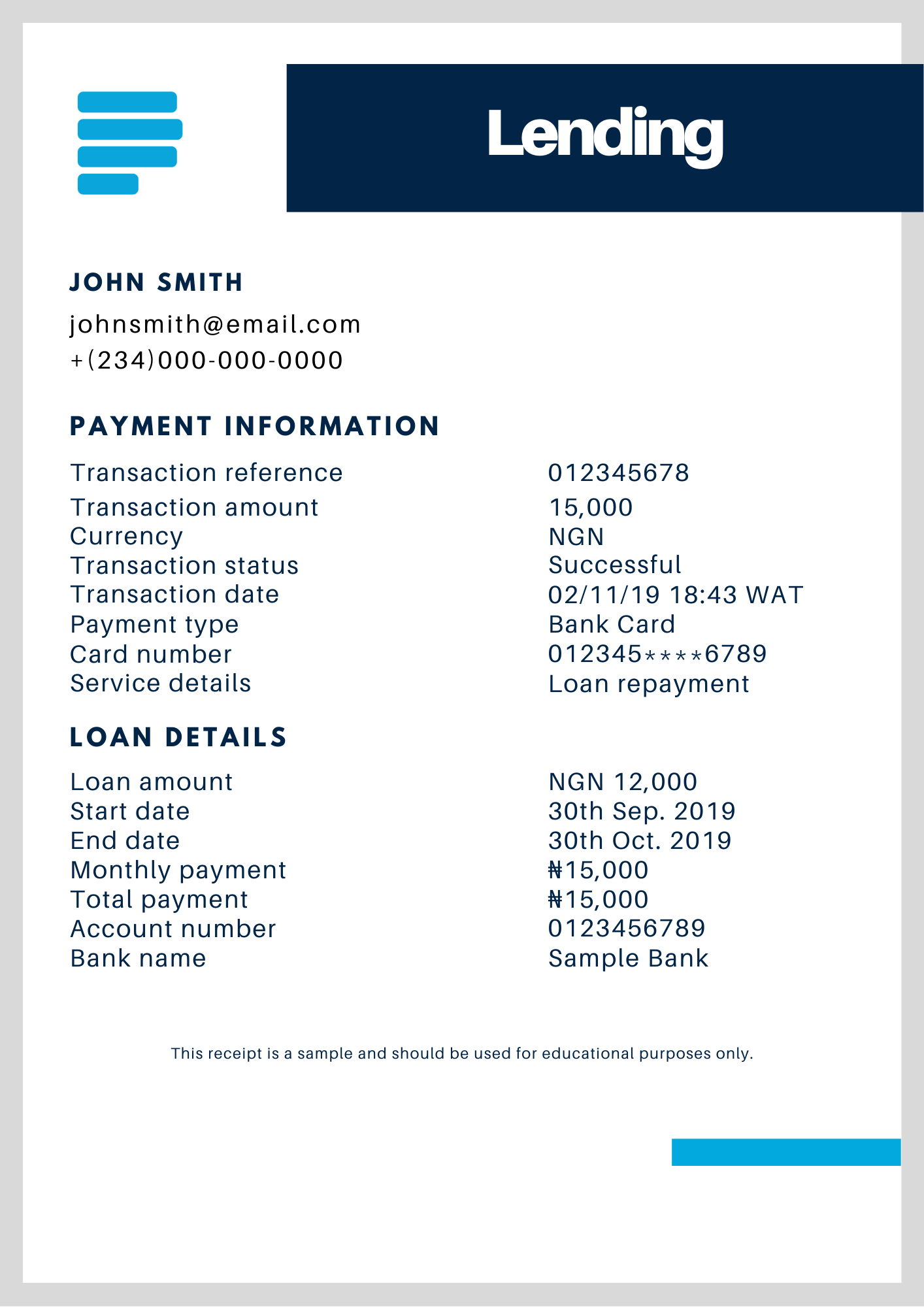

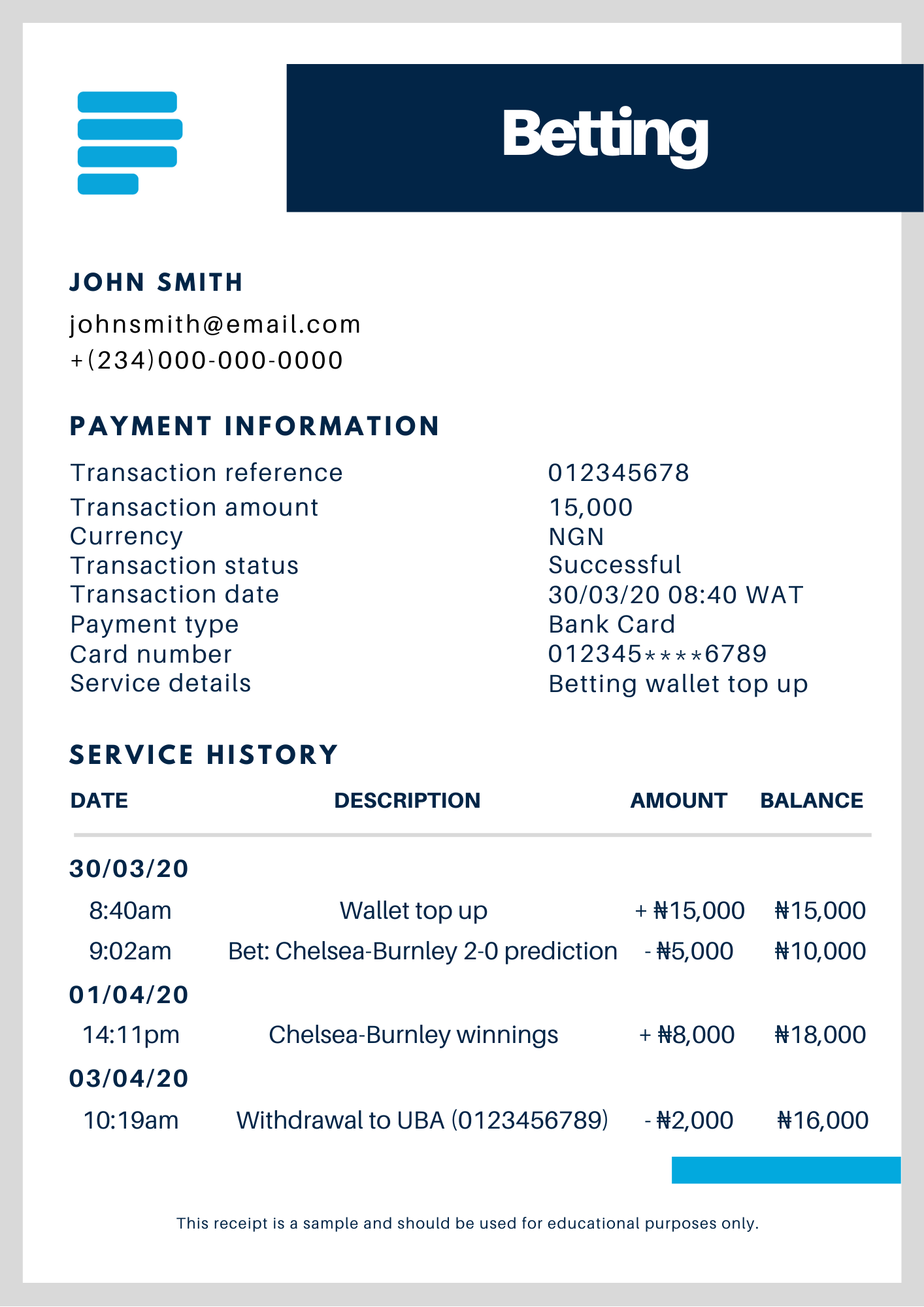

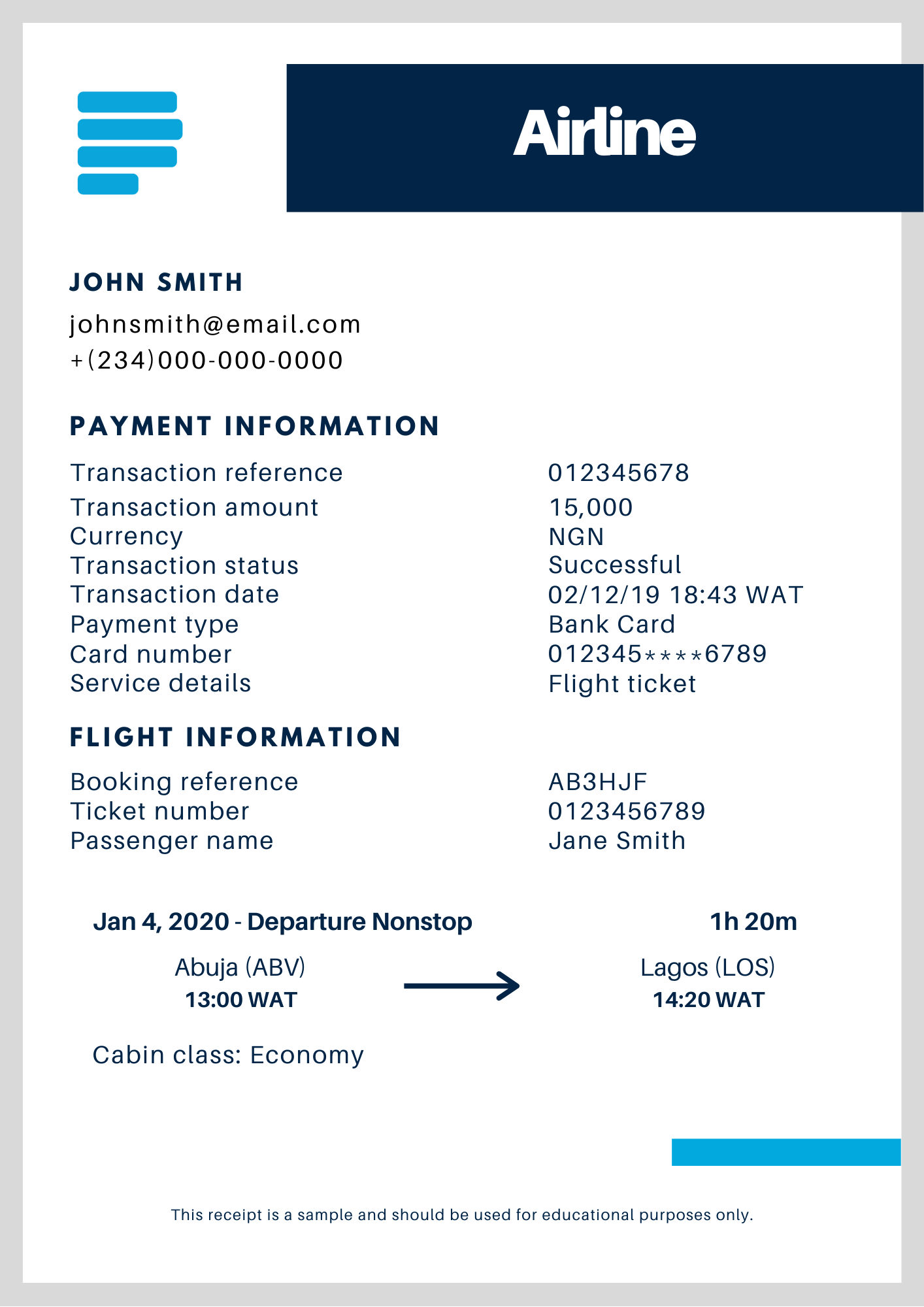

This is an example of a great receipt because it contains even more detailed information on the purchase beyond the customer information

Important to Note:

When providing evidence to decline chargebacks, it is important that it captures the details of the transaction and the customer to be sufficient. Kindly note that text messages and emails citing conversations with the customer will not be sufficient to decline chargebacks.

Here is a list of various types of evidence you can use to decline chargebacks, depending on your business, one or more of these will be suitable for you.

- Signed Invoices (electronic or paper)

- Sales receipts (electronic or paper)

- Delivery confirmation documents

- Service usage times, dates, etc

- Proof that a digital product was downloaded by the customer

For some specific industries like lending, savings, gaming, airline and businesses that offer wallet services, there are stricter requirements for the kind of information that should be included on a receipt when declining disputes.

Other essential practices when providing evidence

- Please make sure documents are clear and legible. Illegible documents may not be admissible and could lead to a financial loss if funds are reversed to the customer.

- Where applicable, make sure documents uploaded only contain details about the specific transaction that is being disputed. Please crop out any data that pertains to other transactions and other customers.

- Make sure to upload all relevant documents pertaining to a chargeback the very first time as there may not always be room for the chargeback to be re-opened.

What happens after I decline a dispute?

When you decline a chargeback with evidence that the customer got what they paid for, we send the evidence to the bank. The chargeback is resolved once the customer's bank accepts the evidence you provide.

However, sometimes, the customer's bank does not accept the evidence provided by a merchant. When the bank doesn’t accept the evidence provided, there could be a request to revalidate the transaction, or in some cases, the chargeback will get moved to the pre-arbitration stage. You can read more about pre-arbitration chargebacks here.

A customer's bank can reject a receipt for one of the following reasons:

The receipt does not carry any transaction details:

This means the receipt doesn't show the transaction amount or the payment method. A bank would be unable to tell that the evidence you provided is for the transaction in question.

If the customer's bank rejects a receipt because of this, we'll have to re-open the dispute. The dispute will reappear on your Paystack dashboard and you'll have to respond again. You should respond with a more detailed receipt. If the bank rejects your response again, the dispute defaults and the customer will get a refund. We deduct the amount of the refund from your next payout.

The customer insists that they didn't get what they paid for:

In this case, the first receipt might already have all the transaction details. To resolve a dispute like this, you'll have to provide some more information to prove that you gave value.

- a signed copy of a physical receipt; and/or

- a copy of the delivery invoice (for physical goods) ; and/or

- a copy of any correspondence received by you from the cardholder.

Once you can provide these documents, we send them to the bank to resolve the revalidation claim or the pre-arbitration chargeback. Based on the evidence you provide, the bank is the arbiter of whether you've proven to have given value or not. If the evidence is enough to prove that you gave the customer value, the resolution is in your favor as a merchant.

If the bank rules that you can't prove that you gave value, the dispute defaults and the customer will get a refund. We deduct the amount of the refund from your next payout.

As long as you're able to provide very detailed receipts as proof that you gave value to your customer, disputed transactions are usually resolved the first time around.

Comments

0 comments

Article is closed for comments.